UIM Coverage in Arizona — Why Every Driver Needs It

If you’re in a Phoenix car accident caused by someone with no insurance — or not enough insurance — who pays for your injuries? If you don’t have UIM coverage, the answer might be: nobody.

What Is UIM/UM Coverage?

Uninsured Motorist (UM) coverage pays for your injuries when the at-fault driver has no insurance at all. Underinsured Motorist (UIM) coverage kicks in when the at-fault driver has insurance, but not enough to cover your damages.

Example: You’re rear-ended on I-10 and suffer $150,000 in injuries. The at-fault driver only carries Arizona’s minimum liability of $25,000. Without UIM coverage, you’re stuck with $125,000 in uncompensated losses. With UIM coverage matching your own policy limits, your insurance covers the gap.

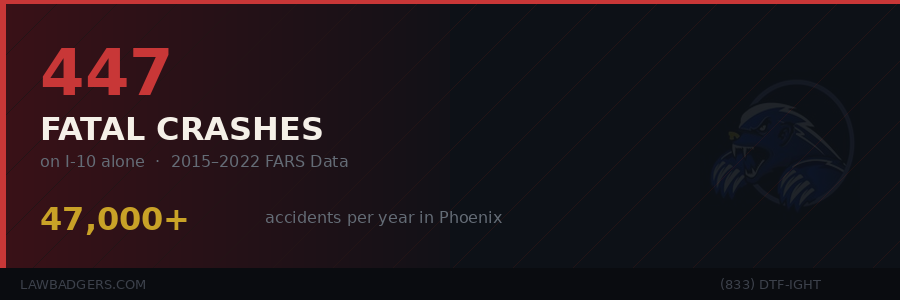

Arizona’s Insurance Landscape

Arizona requires drivers to carry minimum liability coverage of $25,000 per person / $50,000 per accident for bodily injury and $15,000 for property damage. Those minimums haven’t kept pace with medical costs — a single ER visit can exceed $25,000.

Worse, a significant percentage of Arizona drivers have no insurance at all. Arizona consistently ranks among the top states for uninsured drivers. And with roughly 20,000 hit-and-run incidents per year in Phoenix alone, the odds of being hit by someone without coverage are real.

Arizona Law Requires the Offer — But Not the Coverage

Under Arizona law, insurance companies must offer UM/UIM coverage to every policyholder. But you can decline it in writing. Many drivers decline to save money on premiums without understanding what they’re giving up. That’s a gamble the Law Badgers strongly advise against.

How UIM Coverage Works in Practice

When you’re hit by an uninsured or underinsured driver, you file a claim under your own UIM policy. Your insurance company then steps into the at-fault driver’s shoes. Here’s the critical part: your own insurance company is now your adversary. They’re the ones paying, and they’ll try to minimize the payout just like any other insurance company would.

This is exactly why you need an attorney for UIM claims. The Law Badgers have extensive experience fighting our clients’ own insurance companies to get fair UIM settlements.

How Much Coverage Should You Carry?

We recommend carrying UIM limits that match your liability limits. If you have $100,000/$300,000 in liability coverage, carry $100,000/$300,000 in UIM. The cost difference is usually modest — often just $50–100 per year — and the protection is enormous.

If you have significant assets (a home, retirement savings), consider even higher limits or an umbrella policy. The cost of higher UIM limits is one of the best insurance values available.

The Bottom Line

UIM coverage protects you from other people’s bad decisions. In a metro area with 47,000+ accidents per year and tens of thousands of uninsured drivers, it’s not optional — it’s essential. If you’re unsure what coverage you have, pull out your policy declarations page and check. If you don’t have UIM coverage, call your agent today and add it.

And if you’ve already been in an accident with an uninsured or underinsured driver, call the Law Badgers. We’ll fight your own insurance company to get you what you’re owed.

INJURED? GET A FREE CONSULTATION.

The Law Badgers fight for maximum compensation. No fee unless we win.

Call (833) DTF-IGHT